You hire a roofer after a Texas storm damages your roof, expecting them to handle your insurance claim from start to finish. But Texas law strictly prohibits roofers from negotiating claims, interpreting policies, or acting as your representative with insurers. This confusion leads many homeowners into legal trouble or denied claims. Understanding what roofers can and cannot legally do during insurance claims protects your rights, speeds up repairs, and helps you avoid contractors making illegal promises about deductibles or claim outcomes.

Table of Contents

- Key takeaways

- What roofers can and cannot do in Texas insurance claims

- Why many Texas insurance claims for roof damage are denied or unpaid

- How to work effectively with roofers during your insurance claim process

- Comparing roofer services and roles vs. public adjusters in Texas

- Get expert roofing replacement and repair services in Texas

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Claim handling limits | Roofers cannot negotiate claim outcomes, interpret policy language, or act as your representative with insurers in Texas. |

| Public adjuster restriction | Roofers providing contracting services cannot act as public adjusters, and doing so can invalidate your contract and incur penalties. |

| High claim denial risk | Nearly half of Texas homeowners claims close without payment, often due to deductibles or disputes over damage causes. |

| Licensed contractor benefit | Choosing licensed and experienced roofers helps you avoid pitfalls and ensures repairs comply with building codes. |

| Deductible notice rule | Contracts over $1,000 must include a deductible notice, and you should avoid terms that waive deductibles or guarantee insurance approval. |

What roofers can and cannot do in Texas insurance claims

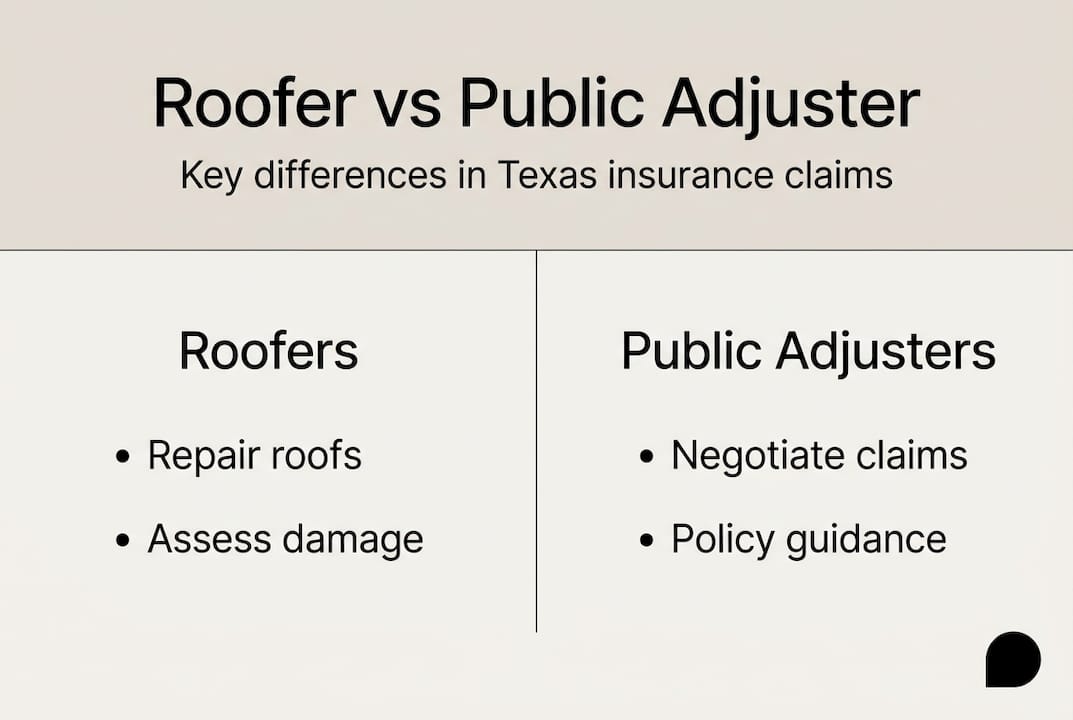

Texas roofers legally provide roofing repair and replacement services, but roofers cannot interpret insurance policy language, advise on coverage decisions, negotiate claim outcomes, act as the homeowner’s representative with the insurer, or promise what insurance will pay. This clear legal boundary protects homeowners from contractors overstepping their authority and making promises they cannot legally keep.

Texas Insurance Code 4102.163 and HB 2102 establish strict rules. Roofers cannot function as public adjusters if they provide contracting services or advertise claims assistance. When a contractor crosses this line, they risk contract invalidation and legal penalties. Property managers and homeowners need to recognize these restrictions upfront to avoid contractors who promise to handle everything.

Contracts exceeding $1,000 must include a deductible notice informing homeowners of their financial responsibility. This requirement protects you from surprise costs and ensures transparency. Illegal contract terms include waiving deductibles, absorbing claim costs, or guaranteeing insurance approval. These promises violate Texas law and should trigger immediate concern.

Pro Tip: Ask potential roofers directly how they handle insurance documentation. Legitimate contractors will explain they provide damage assessments and repair estimates but leave claim negotiations to you or a licensed public adjuster.

What roofers can legally do:

- Inspect roof damage and document findings with photos and measurements

- Provide detailed repair estimates showing labor, materials, and timeline

- Complete repairs according to building codes and manufacturer specifications

- Work with you to schedule inspections and coordinate with your timeline

- Answer technical questions about roofing materials, installation methods, and warranties

Choosing licensed roofing contractors in Texas who respect these boundaries protects your claim and ensures quality repairs. Understanding insurance coverage for roof repairs helps you set realistic expectations about what your policy covers and what roofers can legally assist with during the process.

Why many Texas insurance claims for roof damage are denied or unpaid

Texas homeowners face significant challenges getting insurance claims paid. 47% of homeowners insurance claims closed without payment in recent years, often due to high deductibles, wear and tear disputes, or costs below deductible. This statistic reveals why understanding claim dynamics matters before starting repairs.

| Claim denial reason | Typical scenario | Financial impact |

|---|---|---|

| High wind/hail deductible | 1-2% of dwelling value | $5,000-$9,000 out of pocket |

| Wear and tear dispute | Insurer claims maintenance neglect | Full claim denial |

| Below deductible threshold | Minor damage repair costs | No insurance payment |

| Coverage exclusion | Gradual damage or specific perils | Homeowner pays entirely |

Wind and hail deductibles commonly range from 1% to 2% of your home’s insured value. For a $500,000 home, this means $5,000 to $10,000 in out-of-pocket costs before insurance pays anything. Many homeowners discover these high deductibles only after filing claims, creating financial stress during an already difficult time.

Insurers frequently dispute whether damage resulted from covered storm events or pre-existing wear and tear. Maintenance issues like deteriorated shingles, clogged gutters, or aging flashing give insurers grounds to deny coverage entirely. This makes regular roof maintenance and documentation critical for future claims.

Small damage repairs often cost less than deductible amounts. When repair estimates come in at $3,000 but your deductible is $5,000, insurance pays nothing. Homeowners still benefit from professional inspections to document damage for potential future claims or larger storm events.

Pro Tip: Photograph your roof condition annually and after major storms. This documentation helps prove storm damage versus wear and tear if you file a claim later.

Common claim complications:

- Insufficient damage documentation leading to insurer disputes

- Delayed claim filing missing policy deadlines

- Incomplete repair estimates causing claim underpayment

- Multiple small claims triggering policy non-renewal

- Contractor estimates conflicting with adjuster assessments

Knowing why roofs fail in Texas helps you identify legitimate storm damage versus maintenance issues. Understanding how weather affects roofing durability prepares you for realistic conversations with insurers about damage causes and coverage.

How to work effectively with roofers during your insurance claim process

Selecting qualified roofers and managing the claim process strategically improves your chances for successful repairs and fair insurance settlements. Property managers should prioritize TDLR-licensed local roofers with insurance experience to mitigate risks like warranty voids or non-renewal from multiple claims. This same advice applies to homeowners navigating storm damage repairs.

Verify every roofer’s Texas Department of Licensing and Regulation license before signing contracts. Check their insurance claim experience by asking for references from recent insurance-related repairs. Experienced contractors understand documentation requirements and work smoothly with adjusters without crossing legal boundaries.

Critical questions to ask potential roofers:

- How do you document storm damage for insurance purposes?

- What role do you play during the claim process?

- Will you provide a detailed written estimate matching insurance requirements?

- How do you handle situations where insurance pays less than your estimate?

- Can you provide references from recent insurance claim projects?

- What happens if the adjuster disputes your damage assessment?

Avoid contractors offering to waive deductibles, pay deductibles, or handle claim negotiations. These practices violate Texas law and put your claim at risk. Legitimate roofers explain that you remain responsible for deductibles and claim management while they focus on quality repairs.

Get detailed written contracts including mandatory deductible notices, complete scope of work, material specifications, timeline, and payment terms. Review contracts carefully before signing. Unclear terms or missing deductible notices signal potential problems.

Pro Tip: Request that your roofer attend the insurance adjuster’s inspection. Their technical expertise helps identify all damage, but they should not negotiate claim amounts or coverage decisions.

Maintain clear communication between your insurer and roofer throughout repairs. Share the roofer’s estimate with your adjuster. Provide the adjuster’s assessment to your roofer. This transparency prevents surprises and helps resolve discrepancies quickly. Understanding the role of roofing contractors in Houston and knowing essential questions to ask roofing contractors in Texas prepares you for productive contractor relationships during stressful claim situations.

Comparing roofer services and roles vs. public adjusters in Texas

Texas law creates clear distinctions between roofers and public adjusters to protect homeowners from conflicts of interest. Roofers provide construction services while public adjusters manage claim negotiations and represent homeowners legally. Texas law prohibits roofers from acting as public adjusters if they provide contracting services, advertising claim adjustment, or waiving deductibles. Violations carry serious legal consequences.

| Role | Primary function | Legal authority | Licensing requirement |

|---|---|---|---|

| Roofer | Repair and replace roofs | Provide estimates and complete repairs | TDLR contractor license |

| Public adjuster | Negotiate insurance claims | Represent homeowner with insurer | Texas Department of Insurance adjuster license |

| Combination (illegal) | Both services simultaneously | None – prohibited by law | Cannot legally operate |

Public adjusters must hold separate licensing from the Texas Department of Insurance and cannot provide contracting services while representing clients in claims. This prevents adjusters from inflating damage assessments to increase their own construction profits. The separation protects homeowners from biased damage evaluations.

Roofers who advertise claim adjustment services, promise to handle insurance negotiations, or offer to waive deductibles violate Texas Insurance Code. These violations can invalidate your contract and expose you to legal complications. Legitimate roofers clearly explain their role stops at providing repair services and documentation.

Contract terms that should raise red flags:

- Promises to pay or waive your insurance deductible

- Guarantees about what insurance will cover or pay

- Offers to negotiate directly with your insurance company

- Advertising that mentions claim adjustment or insurance representation

- Contingency fees based on insurance claim amounts

Violations lead to contract invalidation, potential legal penalties for roofing companies, and complications with your insurance claim. Some homeowners have faced claim denials because their contractor violated these laws, creating coverage disputes.

Understanding these distinctions helps you recognize when contractors cross legal lines. If you need professional claim representation, hire a licensed public adjuster separately from your roofing contractor. This keeps roles clear and protects your interests. Learning how to hire roofing contractors in Texas and understanding contractor roles in Houston prepares you to work within legal boundaries while getting quality repairs.

Get expert roofing replacement and repair services in Texas

Navigating insurance claims and roof repairs requires experienced professionals who understand Texas regulations and weather challenges. Mister ReRoof provides licensed roofing services throughout El Campo and Houston, working within legal boundaries to support your insurance-related repairs with quality workmanship and transparent processes.

Our team specializes in shingle roof replacement in Sugar Land, metal roof replacement in Victoria, and TPO roof replacement in El Campo. Each service meets Texas building codes and manufacturer specifications for long-lasting protection against harsh weather conditions.

We provide detailed damage documentation, accurate repair estimates, and professional installations that insurance adjusters respect. Our experience with insurance-related repairs helps streamline your claim process while maintaining the legal boundaries that protect your interests. Contact Mister ReRoof today for a free estimate and discover how proper roofing expertise supports successful insurance claims and quality repairs.

Frequently asked questions

Can roofers help me file an insurance claim for roof damage?

Roofers can document damage through photos, measurements, and detailed repair estimates, but they cannot act as public adjusters or negotiate claims for homeowners in Texas. You remain responsible for filing and managing your claim directly with your insurance company. If you want professional representation during claim negotiations, hire a licensed public adjuster separately from your roofing contractor to maintain legal compliance and protect your interests.

What should I look for when hiring a roofer for an insurance-covered repair?

Verify the contractor holds a valid Texas Department of Licensing and Regulation license and has specific experience with insurance-related repairs. Choose TDLR-licensed roofers experienced with insurance claims to avoid risks like warranty issues or claim denials. Ensure contracts include mandatory deductible notices and clearly define the scope of work, materials, timeline, and payment terms. Avoid any roofer who promises to negotiate with your insurer, waive deductibles, or guarantee claim approvals, as these practices violate Texas law.

Why do some insurance claims for roof damage get denied or not paid?

Many claims receive no payment because high deductibles, wear and tear disputes, or damage costs below the deductible often cause claim denials in Texas. Wind and hail deductibles typically range from 1% to 2% of your home’s value, creating $5,000 to $9,000 out-of-pocket costs before coverage begins. Insurers also deny claims when damage appears related to maintenance neglect rather than covered storm events. Understanding these common issues helps you prepare stronger claims with better documentation.

How much does a typical wind and hail deductible cost in Texas?

Wind and hail deductibles in Texas commonly equal 1% to 2% of your home’s insured dwelling value. For a home insured at $400,000, this means $4,000 to $8,000 in out-of-pocket costs before insurance coverage applies. These percentage-based deductibles differ from flat-amount deductibles for other perils and often surprise homeowners during claim filing. Review your policy declarations page to confirm your specific deductible amounts before storm season.

What documentation should I gather before filing a roof damage claim?

Photograph your roof from multiple angles immediately after storm damage, capturing close-ups of specific damage like missing shingles, dents, or cracks. Document the date and nature of the storm event through weather reports or news coverage. Collect any previous roof inspection reports, maintenance records, and warranty information. Obtain a detailed estimate from a licensed roofer showing damage extent, repair scope, and costs. This comprehensive documentation strengthens your claim and helps counter insurer disputes about damage causes or repair necessity.